How to Build a Payment App? All You Need to Know

- First Things First: What Kind of Payment App Works for You?

- How to Create a Payment App: A Step-by-Step Process

- Key Features of a Payment Application

- Core Security and Compliance Standards for Secure Payment Apps

- Security and Compliance Pitfalls to Avoid When Building a Payment App

- Mobile Payment App Monetization Models

- Key Challenges in Building a Payment App and How to Solve Them

- How Much Does It Cost To Make a Payment App

- Payment App Trends That Will Shape the Next Few Years

- Why Build a Payment App with Appinventiv?

- FAQs

Key takeaways:

- The digital payment market is a massive revolution, creating a massive opportunity for businesses and entrepreneurs.

- Security is a must. PCI DSS compliance, data encryption, biometrics, advanced fraud detection, and scalable tech stack are non-negotiable.

- The cost of payment app development ranges between $40,000 and $400,000 for basic to advanced apps. For enterprise-grade apps, the cost can exceed even $600,000.

- Monetization models and user experience must be part of your plan from day one to ensure long-term success.

- The future of payments is intelligent, driven by AI, biometrics, and real-time processing.

Most new payment apps fail long before they reach real users. The problem is rarely the idea. The real issue is that the market is already dominated by platforms that process billions of transactions every single day. Users are not waiting for another payment app. They already have several installed on their phones, and they only switch when a new platform solves a very specific problem that existing apps have ignored.

This is what makes developing a payment application in 2026 much more challenging than it was several years ago. Development is no longer a challenge. It is differentiation. Unless a new app provides only peer-to-peer transfers, QR payments, or other basic wallet functions, it is not readily embraced, even by early users.

The intensity of competition in this space is largely driven by the scale of the opportunity. The McKinsey Global Payments Report notes that the global payments market already generates around $2.5 trillion in annual revenue.

That level of profitability naturally attracts a large number of fintech companies at the same time. It has become a market that almost every new entrant wants to enter, yet only a small number of payment apps manage to move beyond the early stage and build long-term adoption.

This is exactly why building a payment app today requires careful planning before development even begins. The business model, the technology stack, compliance, scalability, and more: each decision made at this stage of the process impacts long-term success.

This blog describes how high-performance payment applications will be developed in 2026 and all that you need to know about before starting development.

Talk to our team to validate your idea before you invest

First Things First: What Kind of Payment App Works for You?

Before you even think about building a digital payment app, you need to first evaluate, “What are your pain points?” “What problems are you solving? What type of payment app do you actually want?” The market is mushrooming with multiple types of apps, and each plays a different game, but it is full of opportunity if you find the right niche. Thus, this initial thinking is the most important part of your entire digital payment app development journey.

Here is a table outlining various types of payment applications and their specific functions to help you make an informed decision.

| Type of Payment App | Purpose | Payment Application Examples |

|---|---|---|

| Peer-to-Peer (P2P) Payment Apps | Allow users to send and receive money between individuals, often for personal transactions. | Venmo, PayPal, Cash App, Zelle |

| Mobile Wallets | Store payment methods (cards, bank accounts) for easier and faster transactions. | Apple Pay, Google Wallet, Samsung Pay |

| E-commerce Payment Systems | Enable businesses to accept payments for goods and services through an online store. | Shopify Payments, WooCommerce, Stripe |

| Cryptocurrency Payment Gateway | Facilitate transactions using digital currencies like Bitcoin or Ethereum. | Coinbase, Binance, BitPay |

| Buy Now, Pay Later Apps | Allow users to make purchases and pay later in installments. | Afterpay, Klarna, Affirm |

| Digital Banking Apps | Offer full banking services, including loans, investments, and payment services. | Revolut, N26, Monzo |

| Subscription Payment Apps | Manage recurring payments for subscription-based services. | Netflix, Spotify, Hulu |

| QR Code Payment Apps | Use QR codes to facilitate quick, contactless payments between buyers and sellers. | Alipay, WeChat Pay, Paytm |

| International Payment Apps | Enable cross-border transactions and currency conversions. | TransferWise, Remitly, WorldRemit |

| Charity Donation Apps | Allow users to donate money to charitable causes through their mobile phones. | GoFundMe, JustGiving, Charitable.org |

| Micro-payment Apps | Handle small payments, often for digital content like apps, music, or games. | Google Play, App Store, Steam |

| Utility Payment Apps | Facilitate payments for utilities like water, electricity, and internet bills. | Paytm, BillDesk, Biller Direct |

| UPI (Unified Payments Interface) | Facilitates real-time inter-bank payments, linking multiple bank accounts into one platform for fast, seamless transactions. | Google Pay, PhonePe, Paytm, BHIM |

| Super Apps | Offer a wide range of services beyond payments, including shopping, food delivery, social networking, and more, often with integrated payments. | WeChat, Grab, Gojek, Paytm (in India) |

Each type has totally different technical requirements, compliance needs, and user expectations. Your choice affects development complexity and how you’ll eventually make money.

Also Read: List of Top 7 Most Frequently Used Mobile Payment Apps

How to Create a Payment App: A Step-by-Step Process

Successful mobile payment app development follows a structured approach. Each phase builds on the previous one, creating a roadmap from concept to launch. Here are the key steps to create a payment app.

Research and Planning

Every successful business payment app starts with thorough research. Competition causes several startups to fall flat. Understanding your market prevents joining this statistic.

- Market Analysis identifies opportunities and gaps in existing solutions. What problems do current apps solve poorly? Where do users express frustration with existing options?

- User Research involves interviews, surveys, and behavioral analysis. Understanding how the target audience currently handles payments reveals insights shaping app design.

- Competitive Analysis examines existing solutions’ strengths and weaknesses. This research informs feature prioritization and helps identify differentiation opportunities.

- Technical Feasibility assessment evaluates whether your vision is technically achievable within budget and timeline constraints.

Choosing the Sourcing Model

Development approach significantly impacts both cost and timeline:

- In-House Development provides maximum control but requires significant investment in talent acquisition and retention. The need for engineers with blockchain, security, AI fraud detection, and compliance expertise can grow your overall payment app development cost significantly.

- Outsourcing App Development reduces costs and provides access to specialized expertise. However, successful outsourcing requires careful vendor selection and project management, though.

- The Hybrid Model combines in-house strategic oversight with outsourced specialized development. This approach is becoming increasingly popular for complex projects.

Designing the UI/UX and App Architecture

Great payment apps feel effortless to use. Users shouldn’t think about technology – they should focus on their task.

- User Experience Design starts with user journey mapping. How do users discover, onboard, and engage with your app? Each interaction should feel natural and necessary.

- User Interface Design translates experience into visual elements. Payment apps require clean, trustworthy designs communicating security and reliability.

- System Architecture defines how different components interact. Microservices architecture offers scalability advantages. Monolithic designs may be simpler for smaller applications.

Development Phase

Development typically follows agile methodologies with iterative releases:

- Backend Development creates server-side logic, database structures, and API endpoints. This foundation must be robust and secure from day one.

- Frontend Development builds the user interface and integrates with backend services. Careful attention to performance and security is crucial.

- Integration connects your app with payment processors, banking APIs, and third-party services. Each integration point requires thorough testing.

Testing

Payment apps require extensive testing due to security and financial implications:

- Functional Testing verifies all features work as intended across different scenarios and edge cases.

- Security Testing identifies vulnerabilities through penetration testing, code analysis, and infrastructure assessment.

- Performance Testing ensures the app performs well under expected load conditions.

- Compliance Testing verifies adherence to PCI DSS, financial regulations, and app store requirements.

Also Read: The Mobile App Testing Strategies that Appinventiv Follows

Deployment

Launching a payment app involves multiple considerations:

- App Store Submission requires compliance with platform-specific guidelines. Payment apps face additional scrutiny during the review process.

- Infrastructure Deployment involves setting up production servers, monitoring systems, and backup procedures.

- Regulatory Approval may be required depending on app functionality and target markets.

Maintenance

Payment apps require ongoing maintenance and updates:

- Security Updates address newly discovered vulnerabilities and threats.

- Feature Updates respond to user feedback and market changes.

- Compliance Monitoring ensures continued adherence to evolving regulations.

- Performance Optimization maintains app responsiveness as usage grows.

Schedule a free strategy session with our FinTech experts and get a custom roadmap for your secure payment solution.

Key Features of a Payment Application

You don’t need every feature under the sun. That just bloats the app and confuses users. What you need is lean, powerful and core features that engage users and drive real results. When we talk about key features of a payment application, we’re talking about trust.

- Account Linking – Account linking is a safe way to link bank accounts, credit cards, and debit cards using financial APIs and real-time verification.

- Money Transfer – This feature enables customers to send, receive and demand money with ease and integration of contacts and confirmation of transactions.

- User Registration and Authentication – This is an email or phone verification, password, profile and biometric log-in features.

- Security Features – Includes PIN protection, multi-factor authentication, fraud and secure data management.

- Transaction History – Shows the detailed history with search and filters, and export to track the finances more effectively.

- QR Code Payments – Enable quick payments without physical contact in physical locations by scanning codes.

- Push Notifications – Dispatches real-time transaction, security updates and account activity alerts.

- Smart AI Chatbots – Processes frequent requests in real-time and directs complicated ones to a human service where necessary.

- KYC Verification – Enables identity control, selfie control and address control by document upload.

The “Advanced” Features that Make a Difference

Advanced payment apps include next-level functionality that drives users and increases their retention rates:

- AI-Based Fraud Detection – ML algorithms are used to anticipate transaction trends in real-time and prevent unauthorized users.

- Investment Trading Features – Investors can invest in stocks, bonds, crypto, or stablecoins directly through the app.

- Cross-border/International Transfers – Currency conversion, settlement and international compliance can create tremendous technical and regulatory complexity.

- Offline Payment Capability – Local transaction storage and sync mechanisms for unreliable networks.

- Biometric & Behavioral Authentication – Fingerprint, facial, voice, and behavioral biometrics provide multi-layered security.

- DeFi/Stablecoin Integration – Users can hold, transfer, or earn yield on decentralized finance (DeFi) assets.

- Embedded Lending, BNPL (Buy Now, Pay Later) – Instant credit or installment payments, credit scoring, risk assessment and regulatory compliance are required.

- Programmable Wallets / Smart Contracts – This allows custom rules to control payments, recurring payments, or escrows.

- Social & Payment Sharing Features – Split bills, request payment, or share transaction news with friends and groups. Increases involvement and retention.

- Multi-Currency Support – Real-time exchange rate and no hidden charges to international users and travelers.

- Merchant Services and POS Integration – Merchants can directly receive payments, manage inventory and sales analytics in the application.

- Agentic AI in Payments – AI agents for payment apps that can automatically manage recurring payments, optimize spending, flag unusual behavior, and even take actions like bill payments or subscription cancellations.

- Budgeting Tools – Help users track spending patterns and set financial goals. These features differentiate payment apps from simple money transfer utilities.

Find out how we built it and what made the project work

Core Security and Compliance Standards for Secure Payment Apps

Security isn’t optional in mobile payment app development. It’s the foundation everything else builds on. Any app that handles financial transactions must follow strict security practices and also meet regulatory requirements that vary by country and payment type.

Here are some of the core security and compliance requirements essential to following during digital payment app development.

PCI DSS Compliance

The major security standard in any application processing card payments is PCI DSS compliance. It is concerned with ensuring the security of cardholder information, network security, and access to confidential systems.

Regular monitoring, testing, and documentation are also part of compliance, and hence security must be integrated into the development process itself rather than inserted at a later stage.

KYC and AML Requirements

To prevent fraud and unlawful operations, payment apps should check the identity of the user and track their financial transactions. This normally entails identity verification, document verification, and transaction monitoring.

These specifications usually impact the onboarding and development processes, particularly for apps used in the United States or across multiple regions.

Data Privacy Regulations

Security protection of user data has become as significant as payment security. The laws like GDPR, CCPA oblige apps to gather only the required information, keep it in a safe place, and provide users with the opportunity to control the ways their data is utilized. Even a legally secure app may create legal problems if it disregards privacy regulations.

Encryption of Data and Secure Infrastructure

Encryption technology will ensure sensitive information stays safe during transmission and when it is stored. Payment applications are usually based on secure communication protocols and high-level encryption to minimize the risk of data exposure. Controlled access, secure servers and secure API communication among systems also form part of secure infrastructure.

Internal control Fraud Detection, and Risk Monitoring

Current payment applications rely on automated systems that track transactions in real time. These systems detect abnormal behaviour, suspicious transactions, or failed payment attempts before they can cause serious damage. Even smaller payment applications now require simple fraud detection to earn users’ trust.

Periodic Security Audit and Compliance Audits

Security and compliance are not a one-time affair. Payment applications should test their systems regularly, review access controls, and refresh their security systems in response to emerging risks. Regular audits can also help ensure that the platform remains compliant with industry standards as regulations and technologies evolve.

Security and Compliance Pitfalls to Avoid When Building a Payment App

Security mistakes in payment apps aren’t just expensive, but also tarnish one’s business reputation, incuring in loss of users’ trust. Even experienced development teams fall into predictable traps that could have been avoided with proper planning. Here are the biggest mistakes we see companies make, and how to sidestep them before they derail your project.

Ignoring Compliance Early On

Are you one of the many businesses that focus solely on building a product and leave compliance for later? This is a fatal mistake. Don’t do that. You must make regulations like KYC (Know Your Customer) and AML (Anti-Money Laundering) an inseparable part of your app’s architecture from day one.

Poor Scalability

Your app might work fine with a thousand users, but what happens when you have a million? An app built without scalability in mind will crash under pressure. This can lead to outages, transaction failures, and a massive loss of user trust. Make scalability an integral part of your payment app development process from day one.

Inadequate Testing

Don’t just test for happy paths. What happens if a user’s phone loses service in the middle of a transaction? What happens if your third-party API is down? Test your app for all the worst-case scenarios before you bring it to the end users.

Weak KYC and Identity Check

Lots of payment apps do not take the complexity of identity verification seriously. Inadequate KYC practices result in fraudulent accounts, increased fraud risk, and potential regulatory fines. Before development, a robust identity verification process, such as biometrics and multi-factor authentication, needs to be scheduled and cannot be added after the product is developed.

Absence of Data Privacy Controls

The apps used to pay are dealing with personal and financial information, so the privacy rules are critical. Provided that the platform gathers excessive data or stores it without ensuring the necessary protection, it can result in legal complications despite the correct functioning of the payment system. Data storage policies and data collection policies should be determined at the beginning of the project.

Inadequate Succession Records and Documentation

Technology is not the only way regulators can grant approval. Most teams are only geared towards development and do not pay attention to audit logs, compliance reports, and security documentation. Even a well-developed payment application can fail to pass compliance tests in the absence of proper documentation.

Too much Reliance on Third-Party Services

Most payment platforms depend on multiple external services, including payment processors, user verification tools, and banking integrations. When such integrations are done without proper planning, they can pose compliance risks and technical instability. All the external integrations should satisfy security and regulatory requirements before joining the platform.

No Ongoing Compliance Monitoring

Monitoring does not stop once the app has been launched. Rules vary, security threats evolve, and users change with the times. Even when the initial launch of payment apps is successful, those that fail to conduct their compliance procedures on a regular basis have to deal with issues in the future.

Avoid the setback before it happens

Mobile Payment App Monetization Models

Building a payment app is just the beginning. Sustainable monetization strategies for a payment app ensure long-term success and continued innovation.

- Transaction Fees: The most common usage is transaction fees, which are typically based on a per-transaction fee. Other apps charge a percentage of all transfers, whilst some charge fixed fees, or both in tiered systems that reward usage and motivate high-end users.

- Interchange Fees: Application fees enable apps to get a share of the charges that a merchant will pay to a credit card company. An application to become a registered payment processor is necessary, introducing regulatory burdens but providing a reliable income stream.

- Premium Features: Premium features adopt a freemium model, with simpler functions made available free of charge, and more sophisticated features sold. This could be business accounts with reporting, increased limits on transactions, priority support and additional security features.

- Interest and Investment Income: Interest and investment income comes from utilizing user balances. Apps can earn float income by holding funds temporarily or offer investment services that allow users to trade stocks, bonds, or crypto, generating fees from trades or management.

- Partnerships and Advertising: Advertising and partnerships are sources of income without charging the user. Apps may practice targeted advertising, revenue sharing with merchants, or receive commissions on financial products, including loans, cards, or insurance.

- Subscription Services: Subscriptions provide consistent and steady revenue. Premium features may be included in monthly or annual plans, business subscriptions include multiple user accounts, more advanced reporting, and API access to enterprise clients.

Key Challenges in Building a Payment App and How to Solve Them

Every payment app faces predictable challenges. Understanding these obstacles and solutions can save months of development time and high costs. Let’s uncover the potential payment app development challenges and their strategic solutions:

Regulatory Compliance

Challenge: Financial regulations vary significantly by country and region. What works in one market may be illegal in another. In the US, mobile payment app development must comply with the army of federal and state regulations.

Solution: Partner with regulatory experts early in the development process. Consider starting with the single market and expanding gradually as you understand compliance requirements.

Security Threats

Challenge: Payment apps are attractive targets for cybercriminals. Cumulative global payment fraud in online payments is poised to amount to $343 billion between 2023 and 2027.

Solution: Implement security as a core design principle, not an afterthought. Regular security audits, penetration testing, and staying current with threat intelligence are essential.

User Trust and Adoption

Challenge: Users must feel confident putting financial information into your app. New payment apps face significant trust barriers, especially when competing with established players.

Solution: Focus on transparency, security certifications, and gradual trust building. Start with low-risk use cases and expand as users become comfortable.

Technical Integration Complexity

Challenge: Integrating with multiple banks, payment processors, and regulatory systems creates technical complexity. Integration becomes an exercise in retrofitting old equipment with new components usually resulting in data silos, delayed transactions, and compatibility nightmares.

Solution: Use established payment processors and banking APIs when possible. Build a modular architecture of a payment application that can adapt to different integration requirements.

Talent Acquisition

Challenge: Good fintech engineers are hard to find. Keeping them? Even harder. Specialized skills required for payment app development command high salaries and offer multiple opportunities.

Solution: Consider hybrid development models combining in-house expertise with specialized contractors. Invest in training existing team members and create compelling work environments that retain talent.

How Much Does It Cost To Make a Payment App

This is the question on every entrepreneur’s mind. Understanding payment app development cost helps plan budgets and set realistic expectations. However, the pricing is not a fixed number. Below is a clear view of estimates, timelines, and key cost drivers.

| Payment App Development Cost Table | ||

|---|---|---|

| Project Complexity | Estimated Cost Range | Development Time |

| Basic Payment App | $40,000 – $100,000 | 4–6 months |

| Intermediate Payment App | $100,000 – $250,000 | 6–9 months |

| Advanced Payment App | $250,000 – $400,000+ | 9–12 months |

| Enterprise-Level Payment App | $400,000 – $600,000+ | 12–18 months |

Key Cost Drivers

Several factors significantly affect the cost of building a payment app. The initial cost variables include:

- The geographic location of the payment app development services provider affects hourly rates. For instance, hourly rates for app development in the US typically hover around $100 per hour, while in Asia the cost ranges around $40-60/hr. only

- Platform Choice impacts costs. Native development for both iOS and Android costs more than single-platform or cross-platform development.

- Integration Complexity increases costs significantly. Each additional payment method, bank integration, and third-party service adds development and testing time.

- Financial Regulatory Requirements in different markets may require specialized compliance features, increasing development costs.

- Team Structure affects costs. In-house teams require salaries, benefits, and equipment. Outsourced teams typically charge project-based fees.

Ongoing Costs (Post-Launch)

Launching is just the beginning. Payment apps require constant investment to be secure, compliant and performant:

- Maintenance & Security Updates: Typically 15–20% of initial development cost annually.

- Compliance Monitoring: The legal and technical departments would track the compliance with the regulatory changes.

- Infrastructure Scaling: Cloud services and DevOps costs rise with user base growth ($2,000 – $20,000+/month).

- Technical Debt Refactoring: The long-term inefficiency is avoided by improvements to the code and fixing bugs.

- App Store Charges: Apple and Google charge 15%-30% of the transaction revenue.

- Customer Support: An increased customer base requires more customer support teams and systems.

Estimation Methods

Trial-and-error methods are not used in online payment transfer app development. Instead, a clearly defined and structured approach is followed.

Work Breakdown Structure (WBS): Adds the hours of work and attempts to estimate the effort.

Parametric Model (COCOMO II): Thousands of lines of code effort (KLOC) and environmental factors computed.

Example:

Three-Point Estimation (PERT): Reduces bias by considering optimistic, most likely, and pessimistic scenarios.

Example:

These models help founders anticipate costs, avoid hidden pitfalls, and plan realistic budgets before development begins.

Payment App Trends That Will Shape the Next Few Years

The fintech industry is a high-speed train, and it’s essential to keep an eye on what is dominating currently and what’s next. Understanding the current, emerging, and future trends will help you build a forward-thinking app that remains relevant.

BNPL Integration is Still Growing

BNPL apps are no longer a niche service at the checkout counter; it is becoming a general credit overlay in numerous areas of commerce. The BNPL industry is rapidly growing worldwide, with giants such as Klarna and Affirm leading, and payment networks and banks incorporating instalment plans into their services. The trend indicates the adoption of instalment-based payments in retail and other trades.

Stablecoins are Set to Gain Genuine Traction

Stablecoins are evolving into a less speculative payment and settlement instrument. As of 2025, data on the volume of stablecoin transactions (such as USDC and USDT) exceeded $4 trillion on-chain, indicating an increase in transaction volume across commerce, cross-border settlements, and treasuries, rather than trading.

Stablecoins are also becoming more significant in global payment infrastructure as enterprises are increasingly applying them to settle near-instantly and manage liquidity across borders.

AI Is Taking Center Stage with Payments

By the year 2026, AI in payments will no longer be superficial; it will have been integrated into payment routing, risk scoring, and fraud management. It helps AI systems analyze trends in real time to minimize false positives, maximize approval rates, and customize the user transaction experience. The trend is an indication of the way payments are being made smarter and with less manual intervention.

Embedded and Invisible Payments Are Reducing Friction

The payment is losing its place as a standalone activity and becoming an integrated part of a user experience. Embedded finance enables transactions without taking consumers out of the context they are already in, whether in an app, marketplace, or service ecosystem.

This will minimize abandonment during checkout and enhance engagement, especially in highly digitalized systems. The change is part of the broader trend toward payments without borders, where UX is the driving force.

SoftPOS and Mobile Acceptance Expand Merchant Reach

POS systems based on software (SoftPOS) are becoming more popular, particularly with smaller merchants who find more affordable methods to accept payment without the use of traditional terminals. By 2030, the NFC payments market is projected to reach $44.8 billion, helping apps expand offline reach and enable fast retail transactions with minimal hardware investment.

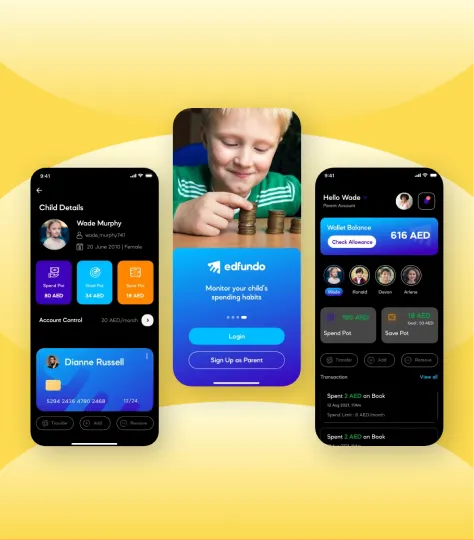

Why Build a Payment App with Appinventiv?

The payment app landscape moves fast, and building something that lasts requires more than just coding skills. You need a team that understands both the technical complexities and the business realities of FinTech app development.

This is where we come in. At Appinventiv, we have helped 3,000+ companies turn their digital ideas into real products, as evidenced by our portfolio. Here is a quick look at how we helped these fintech brands transform their operations.

Edfundo

- $500K secured in pre-seed funding

- $3M seed round prepared

- Scalable platform ready for growth

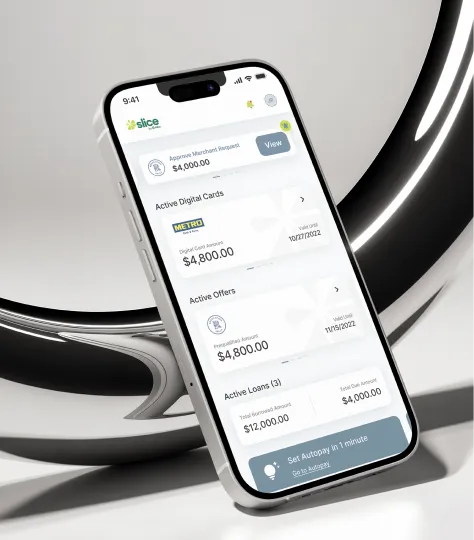

Slice

- Secure and scalable financial backend

- Seamless fractional ownership support

- Launch-ready investment platform

From PCI DSS compliance to user acquisition strategies, our team of 1600+ tech experts specializes in next-gen payment software development that processes millions of transactions safely.

What sets our custom payment apps apart isn’t fancy features, it’s rock-solid architecture that can handle growth. We’ve seen too many promising apps crash under their own success because they weren’t built to scale. Our approach focuses on creating payment systems that work seamlessly, whether you have 1,000 users or 10 million.

From choosing the right tech stack to implementing fraud detection that actually works, we handle the technical heavy lifting so you can focus on building your business. The best part? We know which shortcuts lead to security nightmares down the road.

The fintech space rewards companies that move quickly but thoughtfully. With our ISO certified excellence, regulatory compliance expertise, and deep understanding of what users actually want, we can help you build a payment solution that doesn’t just function; it thrives.

Ready to turn your payment app development idea into reality? Let’s talk about what’s possible.

FAQs

Q. Why create a payment app?

A. The payment app market offers tremendous opportunities driven by changing consumer behavior and technological advancement. These apps have the potential to increase financial inclusion, reduce friction in commerce, and enable new business models that weren’t previously possible. This represents billions of potential users who could benefit from accessible digital payment solutions.

Payment apps also provide multiple revenue streams through transaction fees, premium features, and financial services. The recurring nature of payment transactions creates predictable revenue and high user engagement.

Even if the path of building a payment platform is not easy, the rewards are significant.

Q. How long does it take to go from concept to launch for a payment app?

A. The timeline for secure payment app development varies depending on the project’s complexity and the expertise of the development teams. For instance, a basic MVP development typically takes 4-8 months, while a full-featured payment app requires 8-12 months or more. Complex enterprise apps with extensive integrations may require 12-18 months for full development.

This includes:

- Research and planning: 1-2 months

- Design and architecture: 1-2 months

- Development: 3-6 months

- Testing and compliance: 1-2 months

- Submission and launch: 1 month

Contact a payment app development company to get a more precise estimate for the timeline.

Q. What is the cost of payment app development?

A. On average, the cost of developing a payment processing system ranges between $40,000 and $600,000 or more, based on your unique project requirements and project complexity. For instance,

- Basic apps with MVP-level features cost between – $40,000 and $100,000

- Intermediate-level app development costs range from $100,000 to $250,000

- Enterprise-grade payment apps with futuristic features cost – $250,000 and $400,000+

- Enterprise-grade payment apps with futuristic features cost – $400,000 – $600,000 or more

Discuss your idea with our experts and get a detailed cost estimate tailored to your needs.

Also Read: Cost to Build a FinTech App: What You Need to Know

Q. How to create a mobile payment app?

A. If you are not sure how to create a payment app, here is a step-by-step process to guide you through the journey from concept to code and beyond:

- Research and Planning

- Choosing the Sourcing Model

- Designing the UI/UX and App Architecture

- Development Phase

- Testing and Quality Assurance

- Deployment and Launch

- Maintenance and Upgrade

To gain an in-depth understanding of how to create a payment app, please refer to the above blog.

Q. What measures should we take to ensure regulatory compliance in secure payment app development?

A. Regulatory compliance for building payment app involves multiple requirements:

- PCI DSS Compliance

- Know Your Customer Requirements

- Anti-Money Laundering Compliance

- Data Privacy Regulations like GDPR, CCPA, etc.

These are some of the many payment compliances we adhere to while developing payment apps.

Q. How do we ensure data privacy regulations?

A. Data privacy in payment apps needs solid protection measures. Here’s what works:

- Data Minimization means grabbing only what you actually need and tossing the rest when you’re done with it. Don’t hoard user info just because you can.

- Encryption keeps all sensitive stuff locked down, whether it’s moving between devices or sitting in your database. Use the good algorithms – not the bargain-basement ones.

- Access Controls make sure only the right people see user data. Everyone needs proper authentication, no exceptions.

- User Consent lets people know what you’re doing with their info and gives them real control over it. No sneaky fine print.

- Privacy by Design bakes protection into everything from day one instead of slapping it on later like a Band-Aid.

- Regular privacy check-ups and keeping up with new rules help you stay compliant as regulations change.

Q. How can we leverage AI and machine learning for personalized services?

A. AI and ML create real opportunities in payment apps, such as:

- AI Agents for Fraud Detection spots weird transaction patterns instantly, catching actual fraud while cutting down false alarms that annoy users.

- Personalized Services studies spending habits to suggest useful financial products, budget tips, or merchant deals that actually make sense.

- Risk Assessment figures out the right transaction limits and security checks for different users without being a pain.

- Customer Support bots handle basic questions 24/7, saving money while keeping users happy.

- Predictive Analytics guesses what users want next, helping you build better features and find new revenue streams.

Implementing AI means dealing with privacy rules, bias issues, and regulatory headaches. So, ensure to use responsible AI and explainable AI practices.

Q. How can we ensure payment app security?

A. End-to-end payment app development requires multiple protection layers:

- Multi-Factor Authentication mixes passwords, phones, and biometrics for bulletproof account protection.

- End-to-End Encryption locks down data from the user’s phone all the way to your servers and back.

- Regular Security Audits by real pros find weak spots before the bad guys do.

- Secure Coding Practices stop common attacks like SQL injection and cross-site scripting from ever happening.

- Runtime Protection catches and blocks attacks while they’re happening, not after the damage is done.

- Device Security spots jailbroken phones and prevents man-in-the-middle attacks through certificate pinning.

Q. How do we integrate biometric authentication?

A. Biometric authentication boosts both security and user experience. Here is how we implement it in the payment apps:

- Fingerprint Authentication taps into device hardware for quick, secure identity checks.

- Face Recognition works great for hands-free situations where touching the screen isn’t practical.

- Voice Recognition lets users authenticate through phone calls or voice commands.

- Behavioral Biometrics watches how people type and handle their devices for ongoing verification.

Key things to remember:

- Keep biometric data on the device, not your servers

- Always have backup authentication options

- Follow biometric data regulations religiously

- Test on different devices and real-world scenarios

Biometrics should boost other security measures, not replace them entirely.

Q. How do we add real-time notifications?

A. Real-time notifications keep users in the loop while boosting security:

- Transaction Alerts ping users the moment payments go through, fail, or get received.

- Security Notifications warn about suspicious activity, new device logins, or security changes.

- Balance Updates tell users when their money situation changes or gets low.

- Bill Reminders help people stay on top of recurring payments and due dates.

- Promotional Messages share new features, deals, or financial services that might interest them.

- The technical side involves push services (APNs for iOS, FCM for Android), webhooks for live data, and message queues for reliable delivery.

The trick is balancing helpful info with notification overload. Let users control what they get, and make sure every message actually matters.

- In just 2 mins you will get a response

- Your idea is 100% protected by our Non Disclosure Agreement.

How to Develop an Insurance Portal That Integrates CRM, Claims, and Billing Systems

Key takeaways: Insurance portal development succeeds only when CRM, claims, billing, and policy systems are fully integrated in real time. Architecture choice and workflow orchestration determine transaction accuracy and scalability. Security, compliance, and audit traceability must be embedded across all integration layers. Testing and monitoring are essential to prevent reconciliation gaps after launch. Typical development…

How to Build a Digital Wallet App Like X Money: Cost, Features, and Technology Stack

Key Takeaways: Building a wallet like X Money requires more than payment features. It needs identity verification, fraud monitoring, payment gateways, and a secure financial infrastructure. Development costs usually range between $40,000 and $400,000. The final cost depends on features, compliance requirements, payment integrations, and platform scale. Core technologies include mobile frameworks, backend microservices, financial…

How Much Does Accounting Practice Management Software Development Cost in Australia 2026?

Key takeaways: Custom accounting practice management software development in Australia for mid-to-large firms generally falls between AUD 70,000 and AUD 700,000. Key cost drivers in the 2026 landscape include adherence to the Privacy Act 1988, ATO SBR API integrations, STP Phase 2 compliance, and Sovereign Data Residency requirements. A modular architecture and structured development approach…